Introduction

Imagine running a successful company that generates strong revenue, attracts loyal customers, and builds a powerful brand—only to face massive fines, lawsuits, or even shutdown because you overlooked a regulation.

It happens more often than people realize.

That’s why understanding what compliance means in business is not just a legal concern—it’s a strategic necessity.

In simple terms, compliance ensures that a company follows the laws, regulations, standards, and ethical practices required in its industry. But in reality, compliance goes much deeper than simply “following the rules.” It protects businesses from risk, builds trust with customers, strengthens operations, and supports long-term growth.

Whether you run a startup, manage a corporation, work in finance, healthcare, e-commerce, or technology, compliance affects nearly every aspect of your organization.

For example:

- Financial companies must follow anti-money laundering laws.

- Healthcare providers must protect patient data.

- Online businesses must comply with privacy laws.

- Employers must follow labor and workplace regulations.

Without compliance, even profitable businesses can collapse under legal pressure.

In this in-depth guide, you will learn:

- What compliance means in business

- Why compliance is essential for companies

- Different types of compliance requirements

- How businesses implement compliance programs

- Tools and strategies for managing compliance

- Common mistakes companies make

- Practical tips to stay compliant

By the end of this article, you’ll have a clear, practical understanding of business compliance and how organizations use it to stay safe, ethical, and competitive.

Let’s begin with the basics.

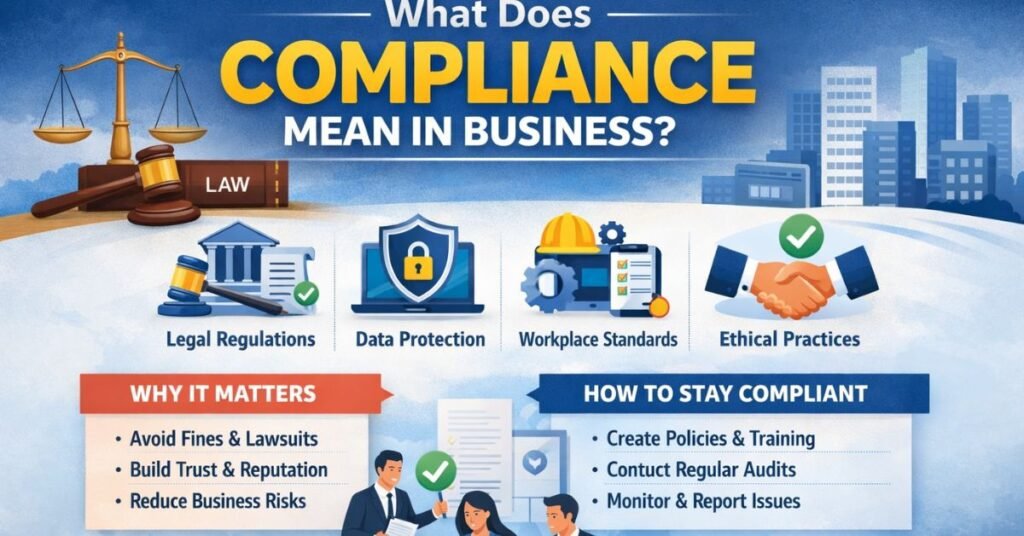

What Does Compliance Mean in Business?

At its core, compliance in business means following the laws, regulations, policies, and ethical standards that apply to a company’s operations.

Compliance ensures that organizations operate legally and responsibly within the framework set by governments, regulatory bodies, and industry standards.

A simple definition:

Compliance in business refers to the process of ensuring that a company follows all applicable legal requirements, industry regulations, internal policies, and ethical guidelines.

This concept applies to businesses of all sizes—from small startups to multinational corporations.

A Simple Real-World Analogy

Think of compliance like traffic laws.

Drivers must follow speed limits, traffic signals, and road rules. These regulations exist to maintain safety and order.

Businesses operate in a similar environment.

Instead of traffic rules, companies must follow:

- Labor laws

- Financial regulations

- Data protection laws

- Environmental standards

- Industry-specific requirements

If drivers ignore traffic laws, accidents occur.

If companies ignore compliance, legal penalties follow.

Key Components of Business Compliance

Business compliance usually includes several areas:

Legal compliance

Companies must follow local, national, and international laws relevant to their operations.

Regulatory compliance

Certain industries are heavily regulated. Companies must follow guidelines set by regulatory agencies.

Corporate compliance

Internal policies ensure employees follow ethical practices and company standards.

Data and privacy compliance

Organizations must protect customer and employee data.

Workplace compliance

Employers must follow labor laws, health and safety standards, and workplace regulations.

Examples of Compliance in Business

To better understand the concept, here are practical examples.

A financial company verifying customer identity to prevent fraud.

A hospital protecting patient records under health privacy laws.

An e-commerce store following consumer protection and data privacy regulations.

A manufacturing company adhering to environmental safety standards.

Each of these actions represents compliance in action.

Compliance vs. Ethics

Compliance is often confused with ethics, but they are not identical.

Compliance focuses on following rules and laws, while ethics focuses on doing what is morally right, even when no law requires it.

Strong organizations combine both:

- Compliance prevents legal problems.

- Ethics build trust and reputation.

Together, they create responsible and sustainable businesses.

Why Compliance Matters in Business

Many entrepreneurs initially view compliance as paperwork or bureaucracy. In reality, it plays a critical role in protecting and strengthening businesses.

Compliance is not just about avoiding penalties—it supports stability, reputation, and long-term success.

1. Avoiding Legal Penalties and Fines

One of the most obvious reasons for compliance is avoiding legal consequences.

Non-compliant businesses may face:

- Government fines

- Legal lawsuits

- Regulatory sanctions

- License suspension

- Business shutdown

For example, companies that violate data privacy regulations may face millions of dollars in penalties.

For many businesses, one major compliance failure can destroy years of growth.

2. Protecting Business Reputation

Trust is one of the most valuable assets a business can have.

Customers, investors, and partners want to work with organizations that operate responsibly.

Compliance demonstrates that a company:

- Respects laws and regulations

- Protects customer data

- Maintains ethical standards

- Operates transparently

When companies violate compliance rules, the damage often extends beyond legal fines.

Reputation loss can reduce customer trust and investor confidence.

3. Improving Operational Efficiency

Well-structured compliance programs often improve internal operations.

Compliance frameworks typically require:

- Standardized processes

- Documentation

- Risk management procedures

- Employee training

- Clear accountability

These systems create better organization and reduce operational chaos.

4. Reducing Business Risks

Every company faces risks such as fraud, data breaches, workplace violations, or financial mismanagement.

Compliance systems help detect and prevent these problems early.

Examples include:

- Internal audits

- Data protection policies

- Financial monitoring systems

- Employee conduct guidelines

By proactively identifying risks, businesses avoid costly crises.

5. Supporting Long-Term Growth

Large investors, partners, and government contracts often require strict compliance standards.

Companies that fail compliance checks may lose opportunities such as:

- Investment funding

- Strategic partnerships

- International expansion

- Government projects

Businesses with strong compliance frameworks are more likely to scale safely.

Types of Compliance in Business

Compliance is not a single category. It includes multiple areas depending on the industry, location, and type of company.

Understanding these different types helps businesses manage their obligations effectively.

Regulatory Compliance

Regulatory compliance refers to following rules established by government agencies and industry regulators.

Examples include:

- Financial regulations for banks

- Healthcare regulations for hospitals

- Aviation safety regulations for airlines

These regulations are usually strict and heavily enforced.

Failure to comply can result in major fines or license suspension.

Legal Compliance

Legal compliance involves adhering to all applicable laws in the regions where a company operates.

This includes laws related to:

- Business licensing

- Taxes

- employment

- contracts

- consumer protection

- intellectual property

Companies operating internationally must comply with laws in multiple jurisdictions.

Data Privacy and Security Compliance

As businesses collect more digital data, privacy regulations have become increasingly important.

Companies must protect sensitive data such as:

- Customer information

- Payment details

- employee records

- medical data

Examples of privacy regulations include global data protection standards and cybersecurity frameworks.

Businesses must implement safeguards like encryption, access controls, and secure storage systems.

Workplace and Labor Compliance

Employers must follow laws that protect workers and maintain fair workplaces.

Workplace compliance includes:

- Minimum wage regulations

- workplace safety standards

- anti-discrimination laws

- overtime regulations

- employee benefits requirements

Companies must also maintain accurate employee records and workplace policies.

Environmental Compliance

Many industries must follow environmental regulations that limit pollution and protect natural resources.

Examples include:

- Waste disposal regulations

- emissions standards

- chemical handling rules

- environmental impact reporting

Manufacturing, construction, and energy industries are particularly affected by these regulations.

Financial Compliance

Financial compliance ensures businesses maintain transparent and accurate financial practices.

This includes:

- accounting standards

- financial reporting

- anti-fraud measures

- anti-money laundering regulations

Companies must maintain accurate financial records and undergo audits when required.

How Businesses Implement Compliance Programs

Compliance does not happen automatically. Companies must build structured systems to ensure ongoing adherence to regulations.

A compliance program is a framework that helps organizations monitor and enforce regulatory requirements.

Step 1: Identify Applicable Regulations

The first step is determining which laws and regulations apply to the business.

This depends on factors such as:

- industry

- company size

- geographic location

- data handling practices

- workforce structure

Companies often consult legal experts or compliance specialists to map relevant regulations.

Step 2: Conduct a Risk Assessment

After identifying regulations, businesses evaluate potential risks.

This includes examining:

- financial risks

- operational risks

- legal exposure

- data security vulnerabilities

- employee conduct risks

Risk assessments help prioritize the most critical compliance areas.

Step 3: Develop Policies and Procedures

Organizations must create internal policies that guide employee behavior.

Common policies include:

- code of conduct

- data protection policies

- anti-fraud policies

- workplace safety procedures

- financial reporting standards

These policies translate regulatory requirements into practical instructions.

Step 4: Train Employees

Compliance policies are ineffective if employees do not understand them.

Training programs help staff learn:

- company rules

- legal responsibilities

- ethical standards

- reporting procedures

Regular training ensures employees stay aware of changing regulations.

Step 5: Monitor and Audit Compliance

Businesses must continuously monitor compliance performance.

This can include:

- internal audits

- compliance reviews

- data monitoring

- risk assessments

Monitoring helps detect issues early.

Step 6: Implement Reporting Systems

Employees must have safe ways to report compliance violations.

Whistleblower systems allow workers to report concerns confidentially.

This encourages transparency and accountability.

Step 7: Update Compliance Programs

Regulations change regularly.

Companies must review and update their compliance programs to reflect new laws and industry standards.

Tools and Software for Managing Compliance

Managing compliance manually can be overwhelming, especially for growing organizations.

Fortunately, many tools help businesses automate compliance management.

Compliance Management Platforms

Compliance software helps organizations track regulations, monitor risks, and maintain documentation.

Popular platforms often include features like:

- regulatory tracking

- policy management

- audit tools

- risk assessments

- employee training systems

These tools centralize compliance processes.

Risk Management Software

Risk management tools help companies identify potential threats before they become serious problems.

These platforms track operational, legal, and cybersecurity risks.

They also provide dashboards and analytics that help leaders make informed decisions.

Data Protection Tools

Businesses that handle sensitive data must implement security tools such as:

- encryption software

- access management systems

- cybersecurity monitoring tools

- secure cloud storage

These tools protect both customer and corporate data.

Free vs Paid Compliance Solutions

Free tools are often suitable for small businesses with limited compliance requirements.

Examples include basic document management systems and policy templates.

Paid compliance platforms typically offer advanced features such as:

- automated monitoring

- regulatory updates

- audit tracking

- integrated reporting dashboards

Larger organizations usually require enterprise-level compliance software.

Choosing the Right Tool

When selecting compliance tools, businesses should consider:

- industry requirements

- company size

- regulatory complexity

- integration with existing systems

- budget

The right tool simplifies compliance management and reduces risk.

Common Compliance Mistakes Businesses Make

Even experienced organizations can struggle with compliance. Many violations occur not because of intentional misconduct but due to poor systems or misunderstandings.

Understanding these common mistakes can help businesses avoid costly errors.

Ignoring Compliance Until a Problem Appears

One of the biggest mistakes companies make is treating compliance as a reactive process rather than a proactive strategy.

Some businesses only address compliance when they receive a warning, complaint, or regulatory inquiry. By that point, the issue may already have caused legal exposure or financial damage.

A proactive compliance culture means:

- Regular audits

- Continuous monitoring

- Ongoing policy reviews

- Early risk identification

Organizations that integrate compliance into daily operations prevent issues before they escalate.

Lack of Clear Policies

Another common problem is vague or outdated policies.

Employees cannot follow rules that are unclear or poorly documented. Many companies have compliance policies hidden in lengthy manuals that staff rarely read.

Effective compliance policies should be:

- Easy to understand

- Accessible to employees

- Updated regularly

- Supported by training

Clear communication dramatically improves compliance performance.

Poor Employee Training

Employees are often the first line of defense against compliance violations.

Without proper training, workers may unknowingly break rules related to:

- data handling

- workplace conduct

- financial reporting

- cybersecurity

Training programs should be continuous rather than one-time events.

Companies often conduct annual compliance training to reinforce knowledge.

Weak Documentation

Documentation is essential in compliance.

If regulators investigate a company, documentation proves that policies and procedures were followed.

Many businesses fail to maintain proper records such as:

- audit reports

- employee training records

- compliance certifications

- policy updates

Strong documentation protects organizations during audits and legal disputes.

Failure to Monitor Third-Party Partners

Compliance risks do not always originate within a company.

Suppliers, vendors, contractors, and partners can create compliance exposure if they fail to follow regulations.

For example:

- A vendor mishandling customer data

- A supplier violating labor laws

- A partner engaging in unethical practices

Businesses should conduct due diligence and monitor third-party partners regularly.

Real-World Examples of Business Compliance

To truly understand compliance in business, it helps to examine real-world scenarios.

These examples illustrate how compliance practices protect companies and their stakeholders.

Example 1: Data Privacy Compliance in E-Commerce

Online retailers collect large amounts of personal data, including:

- names

- addresses

- payment information

- browsing behavior

To remain compliant with privacy laws, e-commerce businesses implement:

- secure payment systems

- encrypted databases

- transparent privacy policies

- customer data access rights

Companies that fail to protect consumer data may face severe penalties and reputational damage.

Example 2: Workplace Compliance in Corporations

Large organizations must maintain safe and fair workplaces.

Compliance programs typically address issues such as:

- workplace harassment

- discrimination

- safety standards

- employee rights

Companies often provide anonymous reporting systems where employees can report misconduct.

These systems protect employees and reduce legal risks.

Example 3: Financial Compliance in Banking

Banks operate in one of the most regulated industries.

Financial institutions must follow strict rules designed to prevent fraud and financial crime.

Compliance activities include:

- identity verification

- transaction monitoring

- suspicious activity reporting

- anti-money laundering procedures

These processes protect both customers and the financial system.

Example 4: Environmental Compliance in Manufacturing

Manufacturers must comply with environmental regulations related to waste, emissions, and resource usage.

Compliance measures may include:

- pollution monitoring

- waste disposal management

- environmental audits

- sustainability reporting

Failure to follow environmental regulations can result in heavy fines and operational restrictions.

Building a Strong Compliance Culture

Compliance programs succeed when they become part of the company culture.

A culture of compliance encourages ethical behavior, transparency, and accountability throughout the organization.

Leadership Commitment

Leadership plays a critical role in establishing compliance standards.

Executives must demonstrate that compliance is a priority by:

- allocating resources

- supporting training initiatives

- enforcing policies consistently

When leaders model ethical behavior, employees are more likely to follow suit.

Open Communication

Employees should feel comfortable discussing compliance concerns.

Organizations often implement:

- whistleblower hotlines

- anonymous reporting tools

- ethics committees

Open communication helps identify problems early.

Continuous Improvement

Compliance programs should evolve as businesses grow and regulations change.

Regular reviews allow companies to update policies, improve training, and strengthen risk management.

Companies that continuously improve their compliance programs stay ahead of regulatory challenges.

Conclusion

Understanding what compliance means in business is essential for any organization that wants to operate responsibly and sustainably.

Compliance is more than just following laws. It represents a commitment to ethical practices, transparent operations, and responsible risk management.

Businesses that prioritize compliance benefit in several ways:

- Reduced legal risks

- Stronger reputation

- Improved operational efficiency

- Greater customer trust

- Better opportunities for growth

Building an effective compliance program requires planning, education, monitoring, and continuous improvement. From small startups to global corporations, every organization must ensure it follows the rules that govern its industry.

The most successful companies treat compliance not as a burden but as a strategic advantage.

When businesses align their operations with legal and ethical standards, they create safer workplaces, stronger customer relationships, and more resilient organizations.

If you’re building or managing a business, investing in compliance today can prevent serious problems tomorrow.

FAQs

What does compliance mean in business?

Compliance in business means following laws, regulations, industry standards, and internal policies that govern how a company operates.

Why is compliance important for companies?

Compliance protects businesses from legal penalties, improves reputation, reduces risk, and ensures ethical operations.

What are examples of business compliance?

Examples include protecting customer data, following labor laws, meeting financial reporting requirements, and complying with environmental regulations.

What is a compliance program?

A compliance program is a structured system of policies, procedures, training, and monitoring designed to ensure a company follows legal and regulatory requirements.

Who is responsible for compliance in a company?

Responsibility typically falls on compliance officers, legal teams, executives, and managers, but all employees share responsibility for following policies.