If you run a business, you already know that cash management is just as important as generating revenue. Profits can quickly disappear if your money sits idle in a low-interest checking account. That’s where a business CD account comes into play.

So, what is a business CD account? Simply put, it’s a savings tool designed specifically for businesses that allows you to earn higher interest by locking your funds away for a fixed period. Instead of letting cash sit unused, a business CD can turn that idle capital into predictable earnings.

Many business owners overlook CDs because they seem old-fashioned compared to modern investment options. But the truth is, Certificates of Deposit remain one of the safest and most reliable ways for businesses to grow cash reserves without taking on risk.

Think of it as putting a portion of your business savings in a time-locked vault that quietly generates interest.

In this guide, you’ll learn:

- Exactly what a business CD account is

- How it works for companies and entrepreneurs

- The benefits and limitations

- Step-by-step instructions for opening one

- How to choose the best CD options

- Common mistakes business owners make

- Practical strategies for using CDs in business finance

Whether you’re a startup founder, freelancer, or established business owner managing surplus cash, this article will give you a clear, practical understanding of how business CD accounts work and how to use them effectively.

What Is a Business CD Account?

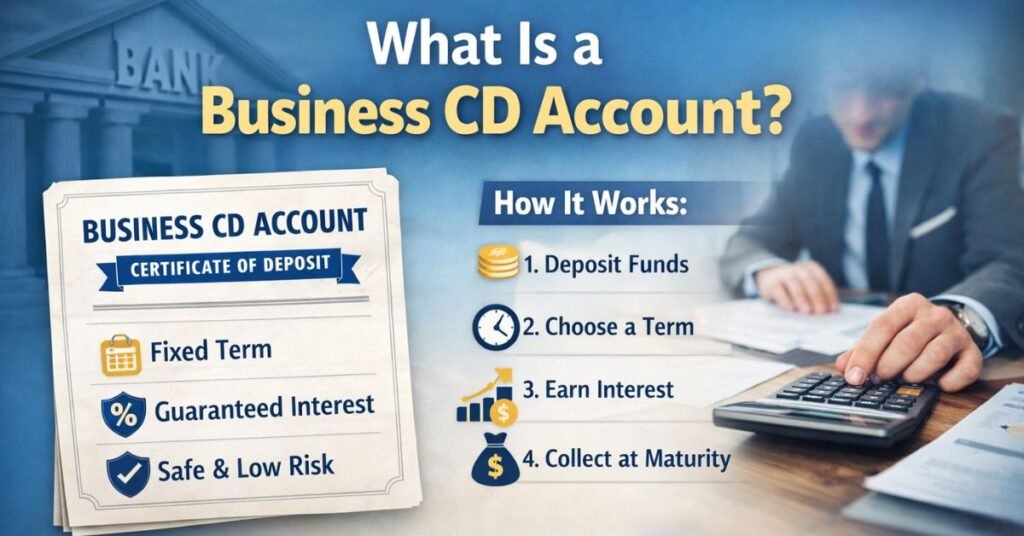

A business CD account (Certificate of Deposit) is a type of savings account designed for businesses where funds are deposited for a fixed period in exchange for a guaranteed interest rate.

Unlike standard business savings accounts, CDs require you to keep the money locked in for a specific term, such as:

- 3 months

- 6 months

- 1 year

- 3 years

- 5 years

During this time, the bank pays you a fixed interest rate, typically higher than a regular savings account.

In other words, the bank rewards you for agreeing not to touch the money for a set period.

A Simple Analogy

Imagine lending money to a friend with the agreement that:

- You won’t ask for it back for one year

- In return, they promise to pay you extra when the year ends

That’s essentially how a CD works.

With a business CD:

- You deposit money into the CD.

- The bank locks the funds for a set term.

- You earn guaranteed interest.

- When the term ends (called maturity), you receive the original deposit plus interest.

Key Characteristics of Business CD Accounts

Here are the defining features that separate business CDs from other business bank accounts.

Fixed Interest Rate

The interest rate is locked in when you open the CD.

Fixed Term

You must keep the funds deposited for the agreed period.

Penalty for Early Withdrawal

Taking money out early usually triggers a fee.

Predictable Returns

You know exactly how much interest you’ll earn.

Low Risk

CDs are typically insured by institutions like the FDIC in the U.S.

Who Can Open a Business CD Account?

Business CDs are available to many types of organizations, including:

- Small businesses

- LLCs

- Corporations

- Partnerships

- Nonprofits

- Sole proprietors

If your business already has a checking or savings account with a bank, opening a CD is usually straightforward.

How a Business CD Account Works

Understanding how a business CD account works is crucial before you commit your company’s cash.

At its core, a business CD operates on three basic elements:

- deposit amount

- interest rate

- time commitment

Let’s break this down step by step.

Step 1: Deposit Business Funds

You start by depositing a lump sum of money into the CD.

Most banks require minimum deposits, often ranging from:

- $500

- $1,000

- $5,000

- $10,000 or more for premium CDs

For businesses with extra cash reserves, this can be an effective place to park funds.

Step 2: Choose a Term Length

The term determines how long the money stays locked in.

Common CD terms include:

- Short-term CDs: 3–12 months

- Medium-term CDs: 1–3 years

- Long-term CDs: 3–5 years

Generally, longer terms offer higher interest rates.

Step 3: Earn Interest Over Time

Once the CD is active, your funds begin earning interest.

Banks typically compound interest:

- daily

- monthly

- quarterly

The interest may be:

- paid monthly

- paid annually

- paid at maturity

Step 4: CD Maturity

When the term ends, the CD matures.

At that point, you have several options:

- withdraw the funds

- renew the CD

- transfer the money to another account

- open a new CD with a different term

Most banks provide a grace period (7–10 days) after maturity to make changes.

Example Scenario

Let’s say your business deposits $20,000 into a 1-year CD with a 4.5% APY.

After one year:

- Your deposit remains $20,000

- Interest earned = about $900

- Total balance = $20,900

That’s money earned with zero market risk.

Benefits of a Business CD Account

Business CD accounts offer several advantages, especially for companies looking to protect capital while earning predictable returns.

Below are the biggest reasons many businesses choose CDs.

Safe and Predictable Earnings

One of the strongest benefits is stability.

Unlike stocks or crypto investments, CDs provide guaranteed returns.

This makes them ideal for businesses that:

- prioritize capital preservation

- want reliable income

- prefer low-risk financial planning

For businesses managing payroll reserves or tax funds, predictable earnings can be extremely valuable.

Higher Interest Than Regular Savings

Business checking accounts often pay little or no interest.

Even business savings accounts typically offer lower rates than CDs.

CDs reward commitment by offering higher yields.

For example:

| Account Type | Typical Rate |

|---|---|

| Business checking | 0–0.1% |

| Business savings | 0.5–1.5% |

| Business CD | 3–5% or higher |

Over time, that difference adds up significantly.

Excellent for Cash Reserve Management

Smart businesses maintain cash reserves for:

- taxes

- emergencies

- seasonal slowdowns

- expansion opportunities

A CD lets you earn interest on those reserves without risking them in volatile investments.

Encourages Financial Discipline

Because CDs lock funds for a fixed period, they discourage unnecessary spending.

This can help business owners maintain financial discipline.

Think of it as a forced savings mechanism.

Flexible Laddering Strategies

Businesses can spread money across multiple CDs with different maturity dates.

This strategy, known as CD laddering, provides:

- consistent liquidity

- higher interest potential

- reduced reinvestment risk

We’ll cover this in detail later.

Who Should Use a Business CD Account?

Not every company benefits from CDs. But for certain situations, they can be extremely effective.

Businesses With Excess Cash

If your company has money sitting idle in a checking account, a CD can turn it into productive capital.

Example:

A marketing agency with $50,000 in reserves could earn thousands annually through CDs.

Companies Saving for Future Expenses

CDs work well when you know exactly when you’ll need the money.

Examples include:

- tax payments

- equipment purchases

- office relocation

- expansion projects

By matching the CD term to the expected expense, you maximize returns without risking liquidity.

Risk-Averse Businesses

Some business owners prefer stable financial tools over market volatility.

CDs are ideal for:

- conservative financial strategies

- businesses protecting operating capital

- nonprofits preserving funds

Seasonal Businesses

Businesses with seasonal revenue cycles often accumulate large cash reserves during peak months.

CDs allow those funds to earn interest during slower periods.

Industries that commonly use CDs include:

- hospitality

- retail

- tourism

- agriculture

Step-by-Step Guide: How to Open a Business CD Account

Opening a business CD account is usually straightforward, especially if your company already works with a bank.

Here’s the complete process.

Step 1: Evaluate Your Cash Flow

Before locking money away, determine:

- how much cash your business can safely deposit

- how long you can leave the funds untouched

Never place funds in a CD that you may need for operations.

Step 2: Compare Banks and CD Rates

Interest rates vary significantly across institutions.

Look at:

- traditional banks

- online banks

- credit unions

Key factors to compare include:

- APY (Annual Percentage Yield)

- minimum deposit requirements

- early withdrawal penalties

- compounding frequency

Online banks often offer the highest rates.

Step 3: Choose the Right CD Term

Your timeline should match your financial goals.

Example:

| Goal | Suggested Term |

|---|---|

| Short-term savings | 3–6 months |

| Tax reserves | 6–12 months |

| Future equipment purchase | 1–2 years |

| Long-term reserves | 3–5 years |

Matching the term to the goal avoids early withdrawal penalties.

Step 4: Gather Business Documentation

Banks typically require:

- Employer Identification Number (EIN)

- business registration documents

- operating agreement (for LLCs)

- business address and contact info

- authorized signer identification

Step 5: Fund the CD

Once approved, deposit the funds.

Funding usually occurs through:

- bank transfer

- wire transfer

- internal transfer from business checking

Step 6: Monitor the CD

Even though CDs are passive, you should track:

- maturity date

- interest earned

- reinvestment options

Setting calendar reminders for maturity dates prevents automatic renewals if you prefer to withdraw funds.

Tools, Comparisons, and Recommendations for Business CDs

Not all CD accounts are created equal. Banks offer a wide variety of CD products designed for different financial goals. Understanding the tools available and how they compare can help you choose the right option for your business.

Traditional Bank CDs vs Online Bank CDs

The first decision most businesses face is whether to open a CD at a traditional brick-and-mortar bank or an online bank.

Traditional banks offer convenience and in-person support. If your business already works with a bank for checking and loans, opening a CD there can simplify financial management.

However, these institutions often offer lower interest rates because they have higher operating costs.

Online banks, on the other hand, frequently provide higher yields because they operate without physical branches. Many businesses are shifting toward online CD accounts for this reason.

Traditional bank CDs typically offer:

- easier integration with existing business accounts

- face-to-face support

- bundled financial services

Online bank CDs often provide:

- higher APYs

- lower fees

- easier rate comparison

The trade-off is that online banking requires full digital account management.

Types of Business CD Products

Banks now offer several variations of CD accounts beyond the traditional fixed-rate model.

Standard CDs

These are the most common type. You deposit funds for a fixed term and receive a fixed interest rate until maturity.

Bump-Up CDs

These allow you to increase your interest rate once during the CD term if rates rise.

No-Penalty CDs

These provide the flexibility to withdraw funds early without paying a penalty, though interest rates are usually lower.

Jumbo CDs

Designed for large deposits, typically $100,000 or more. These often offer higher rates and are popular among larger businesses.

Callable CDs

These allow the bank to terminate the CD early if interest rates change significantly.

Each type serves different financial strategies. For example, a business expecting interest rates to rise might prefer a bump-up CD.

CD Laddering Strategy for Businesses

One powerful strategy businesses use with CDs is called CD laddering.

Instead of locking all funds into a single CD, the money is split across multiple CDs with different maturity dates.

For example:

- $10,000 in a 6-month CD

- $10,000 in a 12-month CD

- $10,000 in an 18-month CD

- $10,000 in a 24-month CD

This structure allows part of the money to become available regularly while still earning higher interest rates on longer terms.

Benefits of CD laddering include:

- improved liquidity

- better interest rate diversification

- consistent reinvestment opportunities

For businesses managing reserves, laddering provides both flexibility and income stability.

How to Choose the Best CD Provider

When evaluating CD accounts, businesses should consider more than just the interest rate.

Important factors include:

Interest Rate (APY)

Even small differences in rates can significantly impact earnings over time.

Minimum Deposit

Some business CDs require large deposits that may not be practical for smaller companies.

Penalty Structure

Understand exactly what happens if you withdraw funds early.

Bank Stability

Choose institutions that are insured and financially reputable.

Customer Support

If your business relies heavily on banking support, access to helpful service matters.

The best CD provider is the one that balances competitive returns with reliable financial infrastructure.

Common Mistakes Businesses Make With CD Accounts (And How to Avoid Them)

Despite their simplicity, business CD accounts can still cause problems when used incorrectly. Many of the mistakes come down to poor planning or misunderstanding how CDs work.

Here are the most common pitfalls and how to avoid them.

Locking Too Much Money Into CDs

One of the biggest mistakes businesses make is placing too much capital into CDs.

Because funds are locked for a fixed period, this can create liquidity problems if the business suddenly needs cash.

For example:

- unexpected tax payments

- equipment failure

- emergency expenses

- growth opportunities

If too much money is tied up in CDs, the business may be forced to withdraw early and pay penalties.

The solution is simple: never lock funds you might need soon. Maintain a healthy operating cash buffer before opening CDs.

Ignoring Early Withdrawal Penalties

CD penalties vary widely across banks, but they can be significant.

Many institutions charge penalties equal to three to twelve months of interest if funds are withdrawn early.

In some cases, the penalty can even reduce the principal balance.

Always review the penalty structure before opening a CD. Understanding the terms protects your business from unpleasant surprises.

Automatically Renewing Without Reviewing Rates

When a CD reaches maturity, many banks automatically renew it for the same term.

While this might seem convenient, it can also trap businesses in lower interest rates if market rates have improved.

Instead, treat each maturity date as a decision point.

Evaluate:

- current interest rates

- business cash needs

- alternative investment options

Sometimes opening a new CD with a different institution produces better returns.

Choosing the Wrong Term Length

Selecting the wrong CD term can limit flexibility or reduce earnings.

For example:

- a 5-year CD may offer a great rate but restrict access to funds for too long

- a 3-month CD may mature too quickly to generate meaningful returns

The best approach is matching the CD term to your financial timeline.

If you plan to purchase equipment in 18 months, choose a CD with a similar maturity.

This alignment ensures the funds are available exactly when needed.

Not Using CD Laddering

Many businesses place all funds into a single CD, which creates a long period with no access to capital.

CD laddering solves this problem by staggering maturity dates.

Businesses that use laddering gain:

- regular liquidity

- consistent reinvestment opportunities

- exposure to changing interest rates

It’s one of the simplest ways to maximize the value of CD accounts.

Overlooking Better Interest Options

Sometimes business owners open CDs with their existing bank simply out of convenience.

However, loyalty can come at a cost.

Online banks and specialized financial institutions often offer significantly higher CD rates.

Before opening a CD, take time to compare offers across multiple providers.

Even a small difference in APY can translate into hundreds or thousands of dollars in additional interest over time.

How Business CD Accounts Fit Into a Smart Financial Strategy

While CDs are not glamorous financial tools, they play an important role in business financial stability.

Think of your business finances as a layered system.

Layer 1: Operating Cash

This includes funds needed for payroll, bills, inventory, and daily expenses.

Layer 2: Short-Term Savings

This money covers upcoming obligations such as taxes or seasonal fluctuations.

Layer 3: Long-Term Reserves

This includes emergency funds or capital for future expansion.

Business CD accounts typically sit in layer two or three.

They are ideal for money that:

- will not be needed immediately

- should remain safe

- should earn predictable interest

For example, a small business might allocate funds like this:

- $20,000 operating cash in checking

- $30,000 short-term reserves in a 6-month CD

- $40,000 long-term reserves in a 2-year CD ladder

This structure protects liquidity while still allowing money to grow.

Another advantage is psychological. When money is locked away in CDs, business owners are less tempted to spend it impulsively.

Over time, this discipline can lead to stronger financial stability.

Conclusion

Understanding what a business CD account is can open the door to smarter financial management for your company.

At its core, a business CD is a simple but powerful tool: you deposit funds, lock them for a set period, and earn guaranteed interest. There’s no market volatility, no complicated strategies, and no risk of losing your principal if the bank is insured.

For businesses with extra cash reserves, CDs offer several advantages:

- predictable earnings

- low risk

- higher interest than savings accounts

- disciplined financial planning

When used strategically — especially through techniques like CD laddering — they can become a valuable component of a company’s financial structure.

That said, CDs work best when they are part of a balanced approach to business finances. Maintaining liquidity, comparing interest rates, and choosing the right terms ensures you get the most benefit from your investment.

If your business currently has cash sitting idle in a low-interest account, exploring business CD options could be a simple way to put that money to work without taking unnecessary risks.

FAQs

What is a business CD account?

A business CD account is a certificate of deposit designed for businesses where funds are deposited for a fixed term in exchange for a guaranteed interest rate. The money remains locked until the maturity date unless the business pays an early withdrawal penalty.

How does a business CD account work?

A business deposits a lump sum into a CD for a specified period. During that time, the bank pays a fixed interest rate. At maturity, the business receives the original deposit plus the earned interest.

Are business CD accounts safe?

Yes. Business CDs are considered low-risk because they provide guaranteed returns. In many countries, deposits are insured by government-backed programs that protect funds up to certain limits.

What is the minimum deposit for a business CD?

Minimum deposits vary by institution. Many banks require between $500 and $10,000, though jumbo CDs may require $100,000 or more.

Can a business withdraw money early from a CD?

Yes, but early withdrawal usually triggers a penalty. The penalty typically equals several months of interest and may reduce the earnings from the CD.